What Executives Are Saying About Private Credit

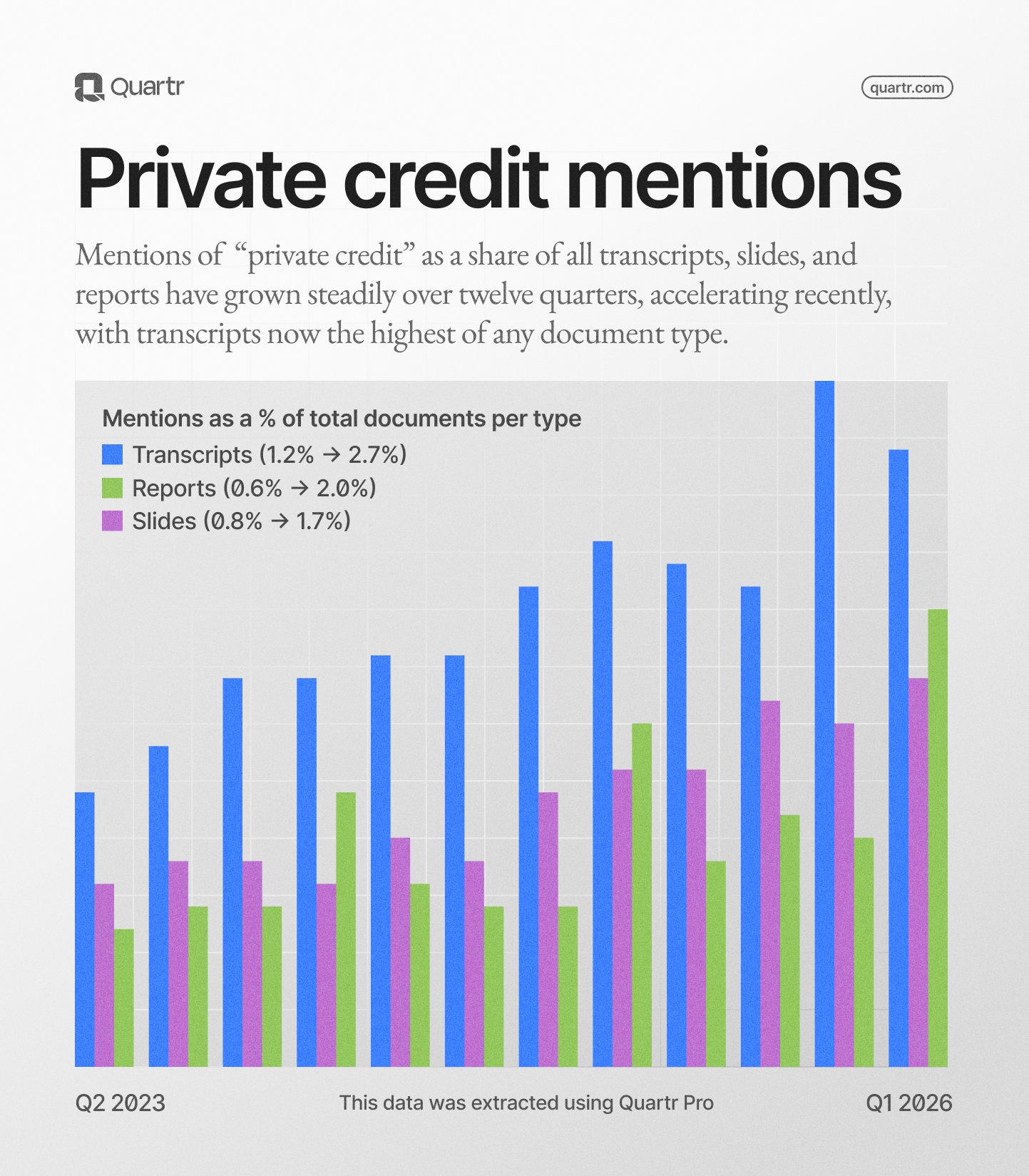

Private credit has grown into a $3 trillion market sitting largely outside regulated banking. Looking at the data in Quartr Pro, mentions of the term across transcripts, slides, and reports have more than doubled since 2023. Over the past two quarters, executives have been unusually direct about conditions in the space. Here is some of what we found.

Overcrowded conditions

SLR Investment's Co-CEO and Co-Founder Michael Gross opened the company's Q4 2025 earnings call with a broad assessment of where private credit stands. Having flagged competitive pressures in sponsor finance for the past two years, he described 2025 as the year the broader market began to catch up:

"The year in hindsight can also be marked as the beginning of a sea change for the maturing private credit industry. Sitting here today, with investor concerns and skepticism running high, we feel relatively insulated from many of the risks facing many of our peers because of our deliberate decision to hold the line with our underwriting standards, particularly in the overcrowded sponsor finance market."

Crescent Capital BDC CEO Jason Breaux described similar conditions on his Q4 2025 call. BDCs, or Business Development Companies, are publicly traded vehicles that lend to mid-sized businesses and must disclose their portfolios quarterly, making them a useful window into private credit conditions more broadly.

"We are operating in an increasingly competitive private credit market. Capital formation across direct lending strategies has remained strong with a growing number of lenders competing for high-quality sponsor-backed transactions. This has resulted in tighter spreads and evolving deal structures."

Redemptions

At the 47th Annual Raymond James Institutional Investor Conference in March 2026, Raymond James CEO Paul Shoukry was asked directly about private credit risk. He drew a distinction between the risk most people focus on and the one he considered more pressing, though he was careful to note he had not yet seen it in the data:

"I think the biggest risk for private credit near term is much less of a credit risk and much more of a funding dynamic in terms of redemptions or ability to raise more funding. Certainly, if the headlines keep coming out around potential cracks and concerns around private credit, that could in itself create concerns and risk, and funding issues for the space."

Private credit portfolios hold illiquid loans that do not price daily. In some of the newer retail-facing structures, the capital behind them comes from vehicles that carry redemption rights, meaning investors can ask for their money back on a set schedule, even when the underlying loans cannot easily be sold.

At the same conference, when asked what investors most underappreciate about MetLife's business, Ramy Tadros, President of U.S. Business, didn't hesitate to address the elephant in the room:

"In weeks like this where there's concerns around things like private credit and risk on the investment side, we have had a philosophy for many, many years to be right down the middle from an investment perspective. What you're hearing about in the market really doesn't apply to us, neither from the asset perspective or the liability perspective."

A real-time read

CLO equity prices daily, private credit loans do not. CLOs, or Collateralized Loan Obligations, are structured vehicles that pool leveraged loans and issue tranches to investors. The equity tranche absorbs losses first but also captures excess returns.

Because CLO equity reprices constantly, it serves as a real-time indicator of stress in the broader leveraged loan market. Laurence Penn, CEO of Ellington Credit, described what that market showed in Q4 2025:

"The fourth calendar quarter was the most challenging market environment for CLO equity since mid-2022 and before that, since the COVID crisis. [...] As estimated by Nomura Research, the median CLO equity return for the quarter was negative 9% and for the full year, negative 14%."

Penn attributed the quarter to elevated credit dispersion, spread compression on stronger credits, and year-end technical selling, and separately flagged growing concern over software sector borrowers facing AI-driven disruption as a headline risk across credit markets entering 2026.

Software exposure

Goldman Sachs BDC Co-CEO Vivek Bantwal gave an update on ARR loan exposure in the company's Q4 2025 call. ARR loans, underwritten against a software company's annual recurring revenue rather than its profitability, became common in private credit during the low-rate era as lenders competed for technology deals.

"Within GSBD specifically, ARR loans came down from nearly 39% of the portfolio on a fair value basis to 11% during that same time period."

Bantwal framed the numbers as progress since GSBD's 2022 reorganisation into Goldman's broader direct lending platform.

Oaktree Specialty Lending CEO Armen Panossian addressed software loans and AI disruption risk during Q1 2026. Asked about the concern among lenders, he explained what he saw as the core issue:

"The concern around the long run calls into question the refinanceability of these loans when they mature. If some number of these software businesses are eventually disrupted by AI, it may turn out to be that they are binary in their outcomes."

Panossian's comments came in the same call in which Oaktree disclosed that Pluralsight, previously restructured in August 2024, had been placed on nonaccrual due to continued industry headwinds and a weaker-than-expected outlook.

PIK interest

Rand Capital CEO Daniel Penberthy noted elevated PIK interest in his Q4 2025 remarks, describing the trend as visible across the BDC industry. PIK, or payment-in-kind, means borrowers pay interest by adding it to the loan balance rather than paying cash, it tends to surface when operating cash flows are too thin to service debt in the normal course.

"Across the broader BDC landscape and to a greater degree in our own portfolio, we have seen continued and elevated use of PIK interest as borrowers manage tighter senior credit conditions."

These are a few excerpts from the past two quarters. Earnings calls are not the only place executives speak candidly; investor conferences, analyst days, and roadshows produce the same kind of disclosure. Most of it receives little attention outside the companies themselves and the analysts who cover them. The volume alone makes it difficult, a single earnings season runs to thousands of calls across public markets. What gets picked up tends to be the numbers. The qualitative detail in those transcripts, how executives describe what they are seeing, what they flag as risk, what language they reach for under pressure, rarely makes it further than the call itself.